Business Loan Agreement Template

Whether you’re borrowing or lending, a business loan agreement provides numerous benefits to both parties.

Updated July 9, 2024

Written by Sara Hostelley | Reviewed by Brooke Davis

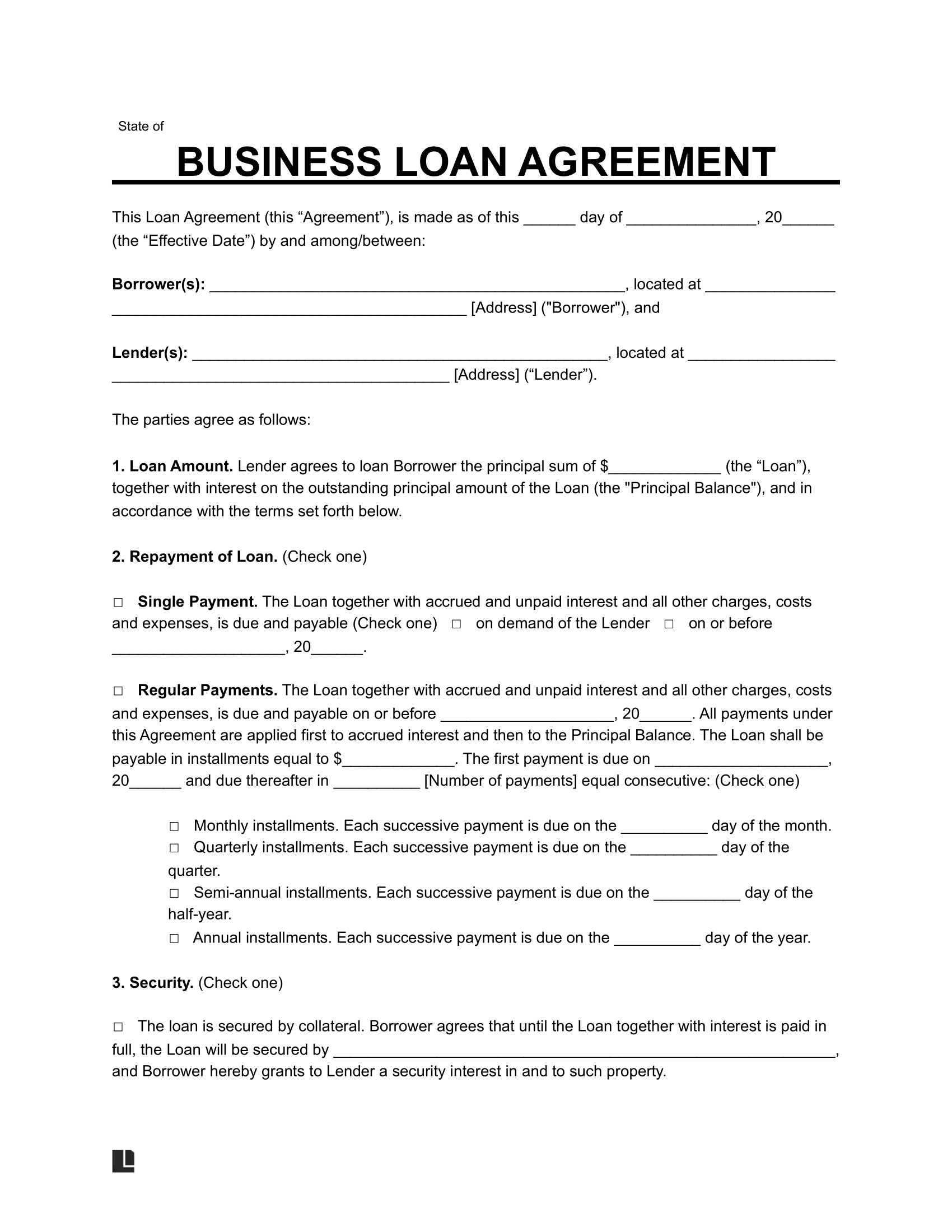

A business loan agreement is a legal contract between a lender and a business borrower that outlines the terms of a loan. It sets out a repayment plan, with interest and other guidelines important to the financial arrangement.

Businesses often need loans to fund their endeavors and build their companies. Lenders need to secure their interests in the money they lend to businesses. In either case, a business loan agreement template can help you build your own.

- What Is a Business Loan Agreement?

- Minimum Requirements For a Business Loan

- Sections of a Business Loan Agreement

- Terms to Know

- How to Write a Business Loan Agreement

- Business Loan Agreement Sample

- Tips to Consider When Writing a Business Loan Agreement

- Disadvantages of Not Using a Business Loan Agreement

- Frequently Asked Questions

What Is a Business Loan Agreement?

A business loan agreement is a document that details the logistical, financial, and legal obligations of the parties to a loan agreement. The business borrower requests money and takes on debt to secure funds.

It details a loan repayment schedule by which the borrower must repay the borrowed funds, including early or default payment conditions. Every business loan is different, but a template helps you get started on the document’s substance while allowing you to modify it to fit your needs.

Types of Loans for Small Businesses

Here are some loan types that small businesses may seek:

Traditional Bank Loans

- Term Loans: They come with a pre-established repayment schedule for a specific amount the borrower repays over a set period.

- Business Lines of Credit: They’re similar to a credit card, letting a business borrow up to a certain limit. They can repay the owed amount and borrow again, paying interest on the amount borrowed.

- Small Business Administration (SBA) Loans: The government provides secured loans to support small business growth. These loans often have a longer repayment term and a smaller downpayment.

Non-Traditional Bank Loans

- Equipment Financing: Businesses use equipment financing to buy equipment, making the equipment collateral for the loan.

- Invoice Financing: With invoice financing, lenders give immediate cash to businesses while using unpaid invoices as collateral.

- Microloan: Community lenders or nonprofit organizations offer small-scale microloans to new businesses with minimal credit history.

When to Use a Business Loan Agreement

Use a business loan agreement whenever a private investor, financial institution, or business entity lends money to a business. It’s wise to use this agreement even with a “small” loan to a friend’s business, as you can prevent disputes over repayment.

Here are some reasons a business may need a business loan:

- To purchase assets (like land, equipment, and machinery)

- To purchase a business (which the buyer can communicate with a business purchase letter of intent)

- To fund a startup

- To cover emergency expenses while waiting for other revenue or financing

- To expand an existing business

- To cover operational expenses or manage cash flow gaps

- To refinance existing debt

Minimum Requirements For a Business Loan

If you want to take out a loan for your business, you must ensure you meet the minimum requirements. Most lenders will require you to fulfill specific criteria before they agree to give you a business loan.

Some of the most critical aspects lenders are going to consider when taking a look at your application include:

1. Credit Scores

If you want to take out a business loan, you must have a solid credit score. First, a lender analyzes your personal credit score. Then, they might also look at your business credit score if you have one.

Generally, credit scores range from 300 to 850. The higher your credit score is, the more suitable you’ll be as an applicant. There are plenty of ways you can improve your credit score. You should pay all your bills on time, keep lengthy lines of credit to lengthen your history, and dispute any inaccuracies on your credit report as soon as possible.

2. Your Annual Revenue

Most lenders will require you to have some revenue stream before providing you with a business loan. Every loan will have different minimums you must meet regarding annual revenue, so you must consider which lender is best for you.

Consider a non-traditional financing option if you don’t have a proven revenue stream.

3. The Years You Have Been in Business

The longer your business history is, the better your chances of qualifying for a business loan. Generally, lenders will require you to be in business for at least two years before providing you with a business loan, but online business loans might have some looser requirements.

4. The Strength of Your Business Proposal or Plan

Before the lender provides a loan, they want to know how you plan to repay the money. That is why your business plan and business proposal are so important.

Your business plan will be responsible for explaining the goals of your business and how you plan to obtain them.

When you put together your business plan, you need to include documents demonstrating you have enough cash to cover the payments on your business loan. This is important for winning the lender’s confidence and maximizing your approval chances.

5. Collateral

You will probably have to provide collateral to back the loan. Essentially, this is an asset the lender can possess if the borrower defaults on the loan. There are different types of collateral, including property, inventory, and equipment.

Collateral is a way for the lender to recover their money if your business fails. You might be able to find an unsecured business loan, but you will probably still have to provide a personal guarantee.

6. Financial Documentation

Finally, you must probably provide extensive documentation to qualify for a business loan. This might include your personal and business income tax returns, a profit and loss statement, a photo of your driver’s license, evidence of any commercial leases you have, your articles of incorporation, and bank statements.

Sections of a Business Loan Agreement

Some of the most important sections that should be included in a business loan agreement include:

- Effective Date: This is the date the agreement takes effect. After this date has passed, the business loan agreement is binding for all parties involved.

- Parties and Their Relationship: This section includes basic demographic information about every party involved, including the borrower and the lender. It will also include your identifying information, address, and how the parties are related.

- Promissory Note or Mortgage: This section includes the agreement to repay the loan.

- Collateral: Collateral is the property or assets the lender seizes if the borrower defaults.

- Terms and Conditions: This section will include the loan amount, the interest rate, and how long the lender must repay the loan. This section will also state whether the lender can pay the loan back early.

- Penalties for Nonpayment: This section will specify what happens if the lender misses a payment. For example, it may determine that the lender must pay a late fee or that there is a grace period during which the lender can make a late payment without being penalized.

- Defaults and Acceleration Clause: This section will spell fines and penalties if the lender cannot repay the loan and defaults. In addition, it could include an acceleration clause. The acceleration clause means that the entire loan balance might be due immediately if the lender doesn’t meet the established requirements.

- Jurisdiction and Governing Law: The law relating to business loans can vary from state to state. This section will specify which rules in which states are responsible for governing the agreement. It may also determine that a specific jurisdiction is to hear any disputes relating to the business loan agreement if there is a disagreement.

- Representations of the Borrower: When a lender takes out a business loan, they must show that they have the legal right to engage in business in the state. This section will also specify that all financial information they have put forth in the agreement is correct and that they comply with all relevant tax laws in the jurisdiction.

- Covenants: Both parties may make specific promises to one another. For example, the lender promises to disperse a certain amount of funds at a specific time. The borrower may promise to purchase insurance for the collateral, provide financial statements periodically, or refrain from taking on additional debt for some time.

Terms to Know

There are several other terms that you might come across as a part of the business loan agreement; they include:

- Amortization: This process refers to the division of the loan repayment into fixed payments over time. As soon as the loan goes into effect, you should be able to get an amortization calendar showing every scheduled payment for the duration of the loan.

- Annual percentage rate (APR): This is the interest rate attached to the loan. It is usually expressed as an annual rate.

- Automated clearing house (ACH): This refers to how your loan payments will be made. Generally, they go through an ACH system to automatically withdraw loan payments from your bank account.

- Balloon payment: A balloon payment is a large, single payment you must make at the end of the loan term.

- Blanket lien: A blanket lien allows the lender to seize any of the borrower’s assets to recoup any outstanding loan balance if the borrower cannot repay the loan.

- Cosigner: A cosigner is another party signing on behalf of the borrower who can improve the chances of the loan being approved. If the primary borrower cannot repay the loan, the cosigner could be responsible.

- Curtailment: A curtailment refers to paying more money than is required monthly. A full curtailment means the borrower pays off the loan in full early.

- Default: Defaulting means that the borrower cannot repay the loan. If the borrower defaults, specific legal processes may kick in on the lender’s behalf to recover the remaining loan balance from the borrower.

- Deferred payment loan: If the payments don’t start immediately, it is called a deferred payment loan. The borrower and lender might agree that the payment process will begin later.

- Factor rate: This is a specific type of business financing expressed as a factor of the total loan amount instead of a traditional interest rate.

- Interest-only payment loan: Some loans only require interest to be paid on the loan instead of the principal. Then, when the loan term is up, the entire principal balance is repaid at once.

- Loan-to-value (LTV) ratio: This ratio refers to the percentage of the asset’s value covered by the loan. This is usually found in real estate when a business needs a loan to purchase commercial property.

- Loan underwriting: This is the process the lender uses to decide the amount of risk that a potential borrower poses to the lender.

- Prepayment penalty: Some lenders will charge a penalty if the lender pays off the loan early. The lender will charge a penalty because they do not collect as much interest on the entire loan. A prepayment penalty compensates for the interest the lender loses on the loan.

- Principal: The principal refers to the amount of the loan. It doesn’t include the interest the borrower will pay on the loan.

- Refinancing: During the refinancing process, a borrower replaces one loan with a different one. Sometimes, borrowers want to refinance their loan because they might be able to get an additional loan at a lower interest rate.

- Servicing: Servicing refers to how the loan is managed. This term covers how funds from the loan will be dispersed, how payments will be collected, and what happens if the borrower doesn’t make the payments on time.

How to Write a Business Loan Agreement

Step 1 – Set an Effective Date

The effective date is when the lender provides the money to the borrower. It establishes the subsequent repayment schedule. Typically, the effective date is the same date the parties sign the document. However, the contract can establish a different effective date.

Step 2 – Identify the Parties

Identify the two parties to the loan agreement. Include the following information about both the lender and the borrower:

- Their names and business names

- The names of officers and signatories to the agreement

- Business and personal addresses, as applicable

- Contact information, including phone numbers and emails

- Service of process information for business entities

- Any cosigner and their information

Step 3 – Include the Loan Amount

Identify the amount in the document when you make or receive a loan. The total amount will help determine how the lender will make future payments and how interest may affect the entire loan. In the beginning, this is the principal amount of the loan before the imposition of any interest.

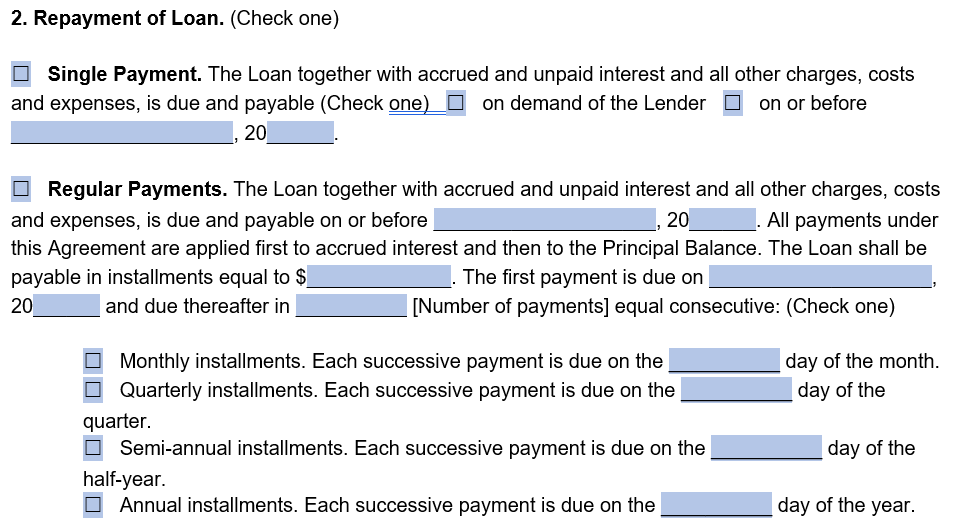

Step 4 – Create a Repayment Schedule

The loan should include when repayment starts and the frequency at which the lender must make the payments. This frequency could be monthly, quarterly, yearly, or any other period. Repayment may begin right away or at a later date.

You may include an amortization schedule in the business loan contract to clearly identify the repayment timeline.

Step 5 – Define Security Interests or Collateral

Many loans will help secure repayment by using collateral. This is some personal property or secured interest in real property that the lender may collect in the case of a default. This is especially common in mortgage agreements.

TIP

You may also want to include the requirement for a guarantor to add security to the business loan agreement.

Step 6 – Set an Interest Rate

The interest rate is the amount the lender charges, in a percentage, of the principal for the loan amount. This amount is essential and is often subject to significant dispute when it’s not clearly defined in a written contract.

Most types of loans require interest for repayment. It is how the lender makes money on the loan. Interest rates are often determined by the current market, the risk of loaning to the borrower, and many other factors. This section should also identify the type of interest rate, such as a fixed or variable interest rate.

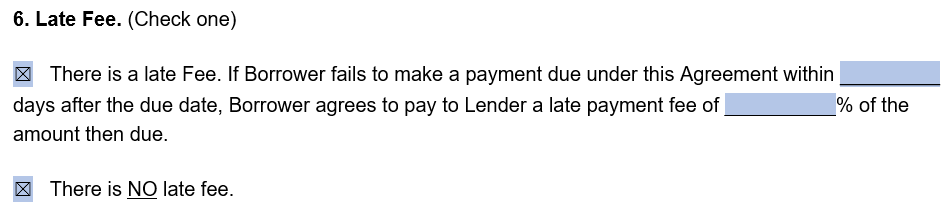

Step 7 – Late Payment Fees

Nearly every loan agreement, especially for business entities, comes with penalties for late payment. Late payments can result in late fees or charges, increases in interest rates, or other methods to deter delayed payments.

TIP

In case of any disputes arising from the agreement, it’s good practice to include how the parties can reach a resolution, such as through court litigation, binding arbitration, or mediation.

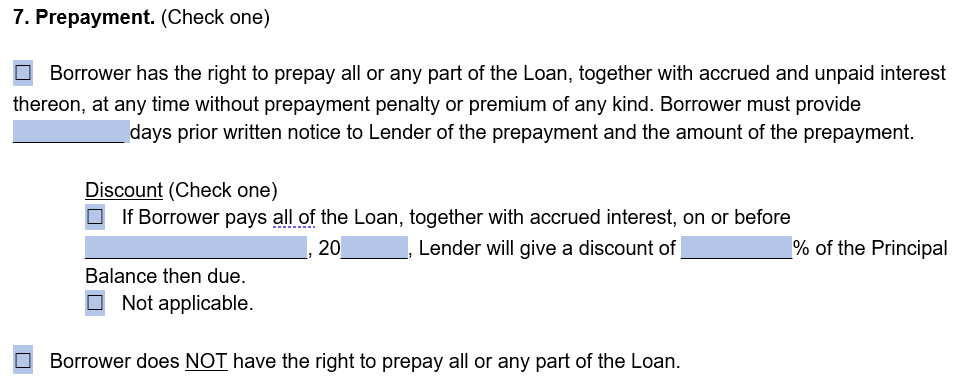

Step 8 – Determine Prepayment Options

The loan may or may not include a prepayment penalty. This creates a fee if the borrower pays off the loan beforehand. Not every loan comes with prepayment penalties.

It is up to the lender whether to include this provision. On the other hand, if the borrower pays all of the loan before a specific date, they could receive a discount.

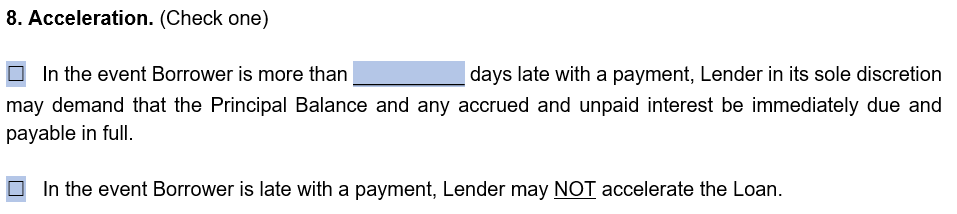

Step 9 – Define the Conditions of a Default

A borrower defaults on a loan when they fail to repay it as the business loan agreement requires. It is crucial to define how a default will be determined. Some loan agreements state that one missed payment may result in a default. Others are much more forgiving.

A default can result in the acceleration of the loan. This means that default makes the entire amount due right away. It also gives the lender a legal right of action against the borrower.

Step 10 – Have a Well-Defined Signature Section

The parties to the loan must sign the agreement to be bound to it. Not only should the business officer sign on behalf of the business, but any personal guarantors or cosigners must also sign at this time. The signature lines should make clear whether the signatory is signing in their capacity or on behalf of the business.

Business Loan Agreement Sample

Download a business loan agreement template as a PDF or Word file below:

Tips to Consider When Writing a Business Loan Agreement

When writing a loan agreement, you should follow a few best practices that can help you create an easy-to-use and enforceable contract:

- Understand key terms: You must know many terms in a business loan agreement. These may include “balloon payment,” “amortization,” and more. Familiarize yourself with these terms so you understand all provisions thoroughly.

- Consider cosigners or guarantors: Many businesses, especially startups, are risky investments. A cosigner or guarantor agrees to pay the loan if the business cannot do so. Personal guarantees can help ensure you get paid for the loan you provided.

- Use appropriate attachments: Many business loans are complex documents. If you want to include additional documents to support the loan agreement, add them to the loan agreement and incorporate them by reference. This might consist of a purchase agreement or other business documents related to the transaction.

Disadvantages of Not Using a Business Loan Agreement

Failing to use a business loan agreement can result in the following disadvantages:

For lenders:

- Lack of enforceability for the loan

- Unclear repayment terms on which you can rely

- Decreased likelihood of timely repayment

- Inconsistent lending standards for customers

For borrowers:

- Unclear expectations about what you owe and when

- Potential for high-cost litigation over the terms of the loan contract

- Possible abuse by a lender in forcing early repayment

- Possibility for higher interest rates or fees than originally agreed

Frequently Asked Questions

Is a business loan agreement legally binding?

Yes, a business loan agreement is a legally binding contract. The court will likely enforce the agreement when all the appropriate information and signatures are included in the contract. A well-drafted agreement can help you ensure that the agreement will be enforced.

What’s the difference between a business loan agreement and a promissory note?

While they are similar, business loan agreements are usually more detailed and need the signature of both the borrower and the lender. Promissory notes spell out a promise to repay a loan but offer little other information relevant to the transaction.

Create Your Business Loan Agreement Today!